Budget 2025 may have sparked some concern amongst kiwis regarding their KiwiSaver investments.

You may be wondering what is happening with the new rules around higher contributions, lower government top-ups, and help for high earners being cut… Here’s what’s really going on, and why KiwiSaver may still be your best long-term investment strategy.

What’s changing from 1 July 2025?

| Change | Before | From 1 July 2025 |

| Minimum employee contribution | 3% of gross salary/wages | Rising gradually to 4% by 2028 |

| Employer contributions | 3% minimum (before ESCT) | Increasing to 4% (by 2028, before ESCT) |

| Government contribution (MTC) | $0.50 per $1 (max $521/year) | $0.25 per $1 (max $261/year) |

| High-income earners ($180k+) | Eligible for MTC | No longer eligible for MTC |

| 16–17-year-olds | No MTC or employer contributions | Eligible for MTC from 2025, employer from 2026 |

What’s new for 16–17-year-olds?

Before:

- No employer contributions

- No government top-up (MTC)

From July 2025:

- Eligible for the government contribution (MTC)

- From 2026, employers will also be required to match contributions for teen workers

Example:

A 17-year-old contributing a minimum of $1,042 per year could receive ~$261 from the government and a close to match from their employer annually, a powerful head start they previously did not have access to.

Over time, even small early regular contributions can make a difference, by compounding into significant long-term savings, potentially even ~$100,000 over 30 years!

The government contribution is halving

The annual government top-up is reducing from $521 to ~$261. Although it’s $260/year less in support, it’s not the full picture! Because you and your employer will be putting in more, your total KiwiSaver savings contributions will still increase.

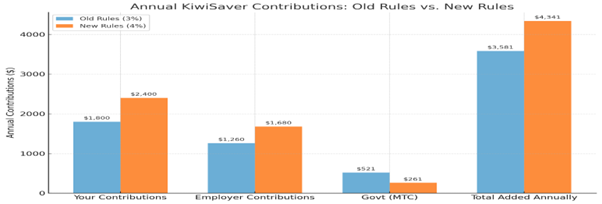

Let’s break it down for someone earning $60,000/year as an example:

Before:

- You contribute: $1,800/year (3%)

- Employer: $1,800 – ESCT = ~$1,260 (30% assumed ESCT)

- Govt (MTC): $521

- Total added annually: $3,581

After (from 2028):

- You contribute: $2,400/year (4%)

- Employer: $2,400 – ESCT = ~$1,680

- Govt (MTC): $261

- Total added annually: $4,341

So, that’s an extra ~$760/year added to your KiwiSaver savings, even with a lower government top-up.

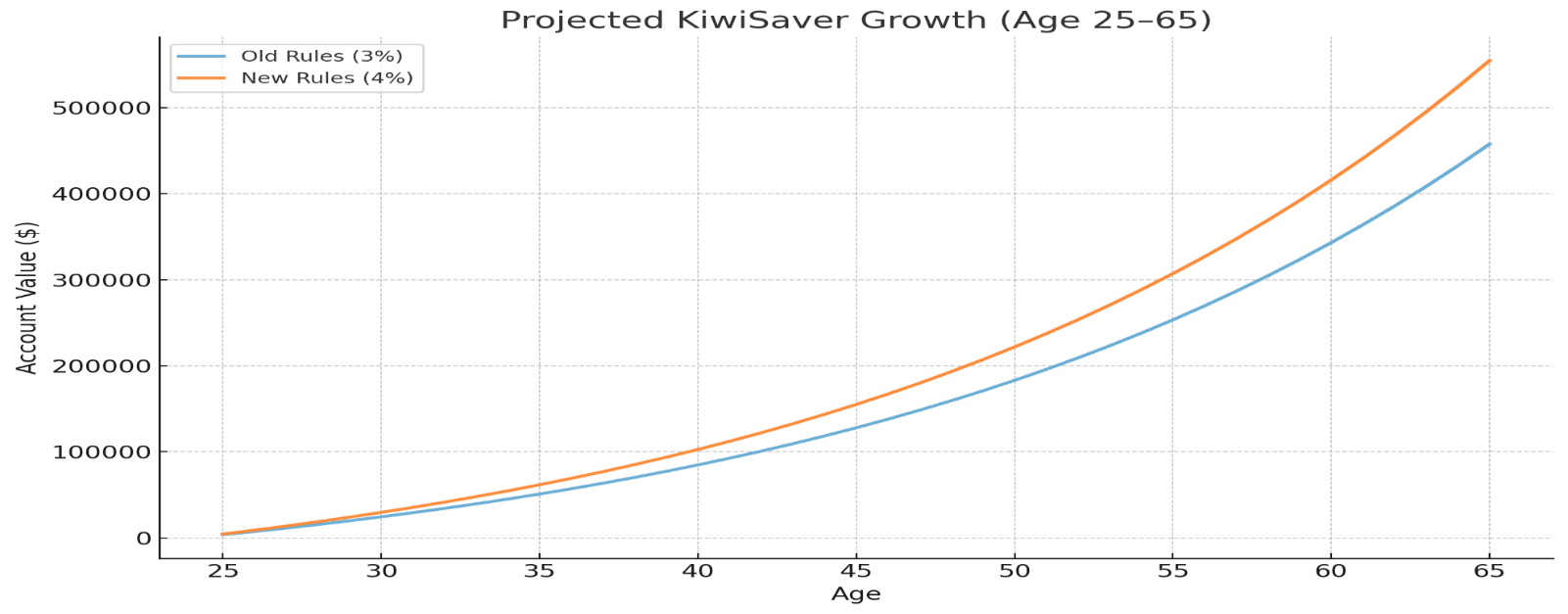

Year-by-year growth: old vs new rules

Value at Retirement (Age 65)

| Scenario | Your Contributions | Estimated Value @ 65 |

| Old Rules | $72,000 | ~$471,000 |

| New Rules | $96,000 | ~$571,000 |

*Assumptions in disclaimer

Even with a halved government top-up, you could finish $100K better off in retirement under the new rules, simply because more money was contributed.

What that extra $100K could mean

That additional $100,000 at retirement could give you:

- $4,000 per year for 25 years

- All on top of NZ Super (if eligible)

That’s potentially money for a holiday, to leave a legacy for your kids, cover future health costs, create a safety buffer, enjoy a comfortable retirement, or simply have more choices in life!

What about high earners ($180k+)?

Even without the government contribution, KiwiSaver still holds major value:

- Employer contributions up to 4% (before ESCT)

- Tax-efficient growth via the PIE regime (lower than top marginal rates)

- Compounding over decades with little admin

If you’re a high-income earner, KiwiSaver may not be your only retirement savings tool, but it’s still one of the most efficient places for long-term compounding.

Final thoughts

Although halving the government contribution may feel like a step back, the bigger picture shows KiwiSaver being rebalanced:

- More from you

- More from your employer

- Still tax-efficient under PIE rules

- Still growing long-term

- Still the #1 retirement tool for most kiwis

What should you do?

- Keep contributing

- Review your fund

- Get advice if unsure

- Encourage teens to join early

KiwiSaver remains one of the easiest ways to turn your $1 into many multiples more over time, with help from your employer, government, and compounding interest.

Even with less government support, your contributions and time in the market still make KiwiSaver a powerful tool to utilise. Be patient, stay the course, and your future self will thank you for it!

Looking to review your KiwiSaver account? Speak to an adviser today to find out how you can make the most of your contributions.

Important disclaimer:

The projections and scenarios provided are for illustrative purposes only. They are based on assumptions that may not reflect actual outcomes. Past performance is not indicative of future returns. Please consult a licensed financial adviser for personalised advice.

Assumptions: We’ve based this projection on a 25-year-old earning $60,000 annually, contributing 4% to KiwiSaver in a high growth fund, with regular contributions and a 6% annual return (before fees and taxes), the model assumes retirement at 65 and drawing income until age 90.

Don't delay, review your KiwiSaver account today!

Fill out the form below and one of our KiwiSaver experts will call you within 24 hours.

"*" indicates required fields