A simple concept often highlighted in investment discussions is the impact of starting early.

Even small, consistent contributions made early in life can create a meaningful head start by the time someone enters the workforce.

Over a lifetime, the difference this creates is far greater than most people expect.

A $30,000 head start.

Or $0.

Same person.

Same salary.

Same contribution rate.

Same assumed return.

The only difference is time.

The comparison

The key variable in this scenario is the starting balance.

- Scenario A begins with $30,000 in KiwiSaver at age 18, built gradually through early contributions.

- Scenario B starts with $0.

Nothing else changes.

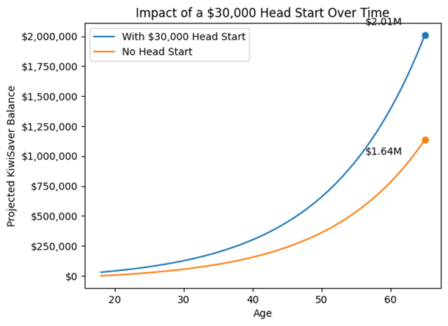

Scenario A: $30,000 head start

By age 65, the projected balance is approximately $2.01 million.

Scenario B: starting from $0

By age 65, the projected balance is approximately $1.64 million.

Assumptions

Two individuals are modelled starting work at age 18:

- Salary: $50,000 per year

- Employee contribution: 3%

- Employer contribution: 3%

- Assumed return: consistent across both scenarios

The difference

This results in a gap of approximately $471,000.

There is:

- No higher investment risk

- No increase in contribution rates later in life

- No difference in salary

The outcome is driven purely by time.

Nearly half a million dollars of additional wealth comes from money invested before the individual even begins earning.

Why this matters

Compounding rarely feels significant in the early years. Growth tends to appear steady and relatively modest.

Over longer timeframes, however, the impact becomes substantial.

Starting earlier allows:

- More time for investments to compound

- Less pressure to contribute aggressively later

- Greater flexibility when approaching retirement

In many cases, wealth creation begins well before someone earns their first income. One of the most powerful advantages in investing is simply getting started earlier than most.

KiwiSaver changes: why reviewing your contributions matters now

From 1 April 2026, KiwiSaver contribution rates are increasing from 3% to 3.5% for both employees and employers, with a further increase to 4% already signalled for 2028.

For many people, this change will happen automatically through payroll, meaning slightly less take-home pay but more going into long-term savings each pay cycle.

While the increase may seem small, even a 0.5% uplift can make a meaningful difference over time as those additional contributions begin compounding.

This makes it a timely opportunity to review your KiwiSaver investment. A contribution increase alone does not guarantee better outcomes, your fund choice, risk level, and overall strategy still play a key role in how your balance grows over time.

Assumptions used in these projections

- Starting age: 18

- Retirement age: 65

- Scenario end age: 90

- Salary: $50,000 per year

- Employee contribution: 3%

- Employer contribution: 3%

- Assumed return: 5.5% per annum

- Figures are nominal and before fees or tax

- Returns are not guaranteed and actual outcomes will vary

These figures are illustrative only and designed to demonstrate the long-term impact of starting earlier.

If you would like to understand how your KiwiSaver investment is tracking, or explore strategies to make the most of these upcoming changes, contact us through the form below to speak with an adviser.

You can also watch our KiwiSaver Webinar, which explores practical ways to improve long-term investment outcomes.

Please fill in the form below with your contact details and one of our advisers will get in touch in 24 hours. "*" indicates required fields

Wherever you are on your investment journey, we can help.